Governance and Trust - The Invisible Variables that Drives the Markets

A talk delivered on 13 March 2026 at the Fund Managers’ Association of the Philippines

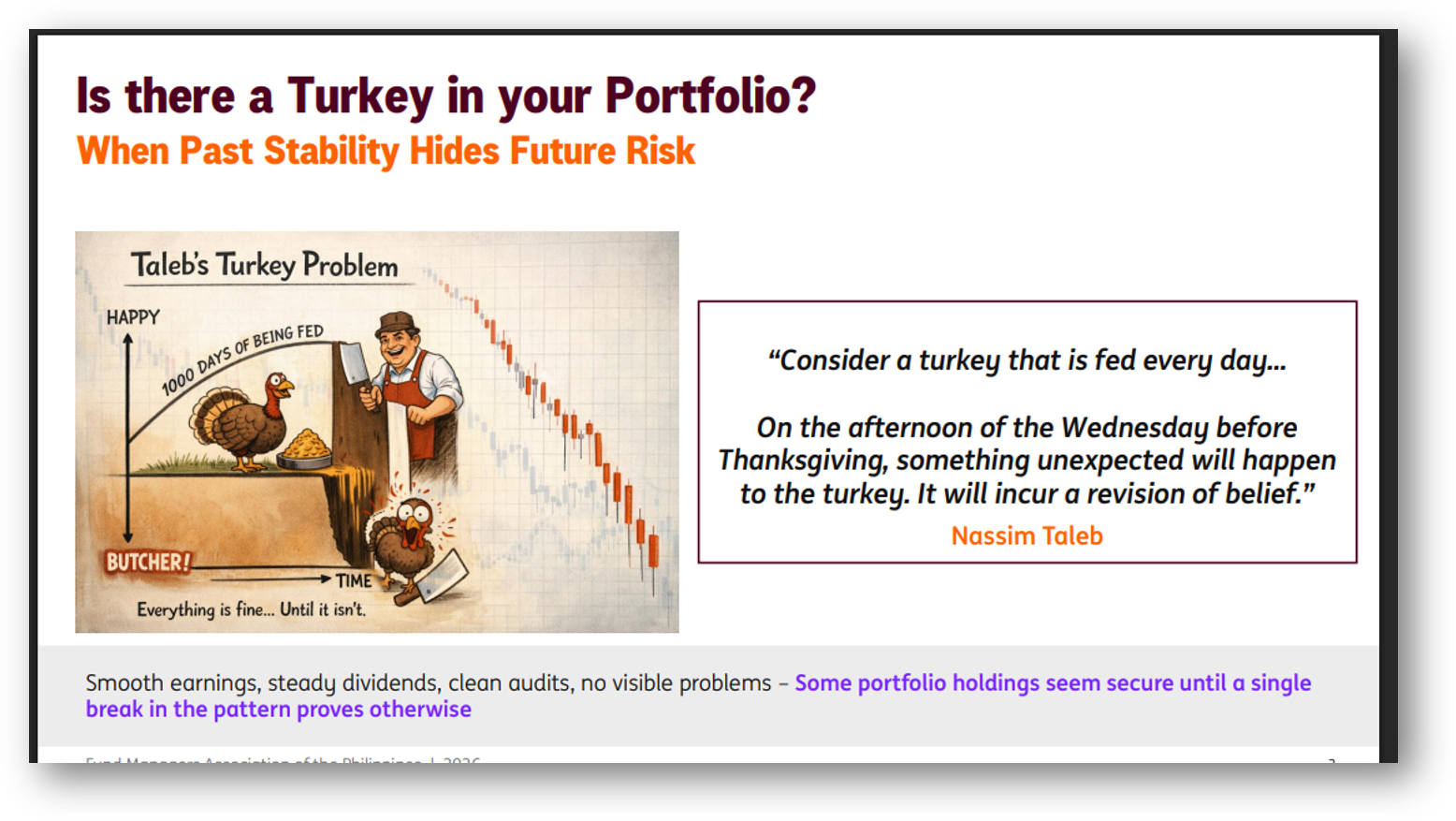

The Story of the Turkey

A turkey lives on a farm. Every morning, the farmer shows up with food. Day one. Day ten. Day one hundred. Day five hundred. The turkey builds a model. The model says: the farmer is my friend. By day nine hundred, confidence is near-perfect. The data is clear. The track record is flawless.

Day one thousand and one is Thanksgiving.

Nassim Taleb tells this story to make a point about hidden risk. One thousand days of evidence gave the turkey zero information about the one day that mattered. The model was not wrong in a small way. It was wrong in a catastrophic way.

Every portfolio has turkeys in it. Companies with clean audits, smooth earnings, steady dividends. No visible problems. The question that separates good investors from everyone else is simple: what does the farmer’s incentive structure look like? And does it align with your survival?

That is a governance question. And it is the question that most models fail to ask.

The Market that Never Forgets

I am a structurer by training. Derivatives, cash flows, credit enhancement, the arithmetic of present value. For most of my career, I have been the person in the room telling clients to focus on the hard numbers. The audited numbers. The discountable numbers. So when I argue that governance and trust are among the most powerful pricing variables in the investable universe, this was not always what I believed in.

Early in my career, I pitched a deal to a listed company that was surging. The economics were sound. The credit had improved from what it had been in the late 1990s. New management. New shareholders. Prominent CEO.

My Chief Risk Officer killed it in thirty seconds. He did not look at the model. He did not challenge the numbers. He said four words: ‘I remember this name.’

Deal dead.

I thought he was being irrational. He was being rational in the deepest sense. He knew something the spreadsheet could not capture: once trust is broken at scale, the cost of rebuilding it is not linear. It is not quadratic. It approaches permanence.

Trust, once destroyed, calcifies into a permanent risk premium. The next generation of management inherits the damage without having committed the original sin. This is not a soft observation. It is a structural feature of how markets process memory. And it has precise, measurable consequences for valuation.

Billions of dollars disappeared in the Jakarta Stock Exchange. Not from a pandemic. Not from a policy error. From trust being violated. That statement deserves more than rhetoric. It deserves a first-principles investigation into how governance and trust translate into prices, and what professional investors can do about it.

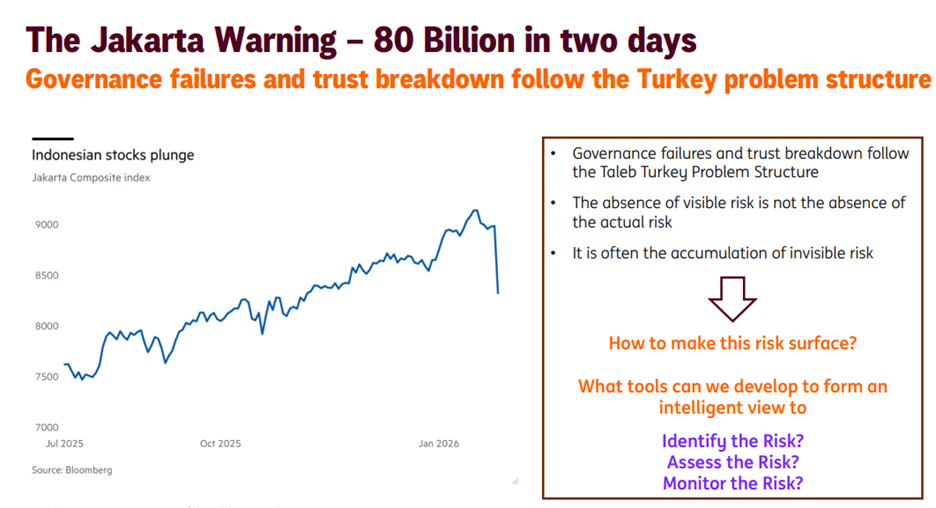

The Jakarta Warning: $80 Billion in Two Days

On January 28, 2026, MSCI froze Indonesia’s rebalancing review and warned of a potential downgrade from Emerging Market to Frontier Market status. The reasons cited: lack of transparency in ownership structures, unreliable free-float data, and concerns about coordinated trading that undermines price formation.

The Jakarta Composite Index fell 7.35% that day. In two days, roughly $80 billion in market capitalization was erased. Foreign investors, who had already pulled 13.96 trillion rupiah out of Indonesian equities in 2025, accelerated their exit. Goldman Sachs and UBS both downgraded Indonesian equities the following morning. The rupiah hit record lows.

The critical question: what actually changed?

Corporate earnings did not change. GDP projections were not revised. The commodity endowment did not shrink. Nothing about the economic fundamentals of Indonesia changed on that day.

One thing changed. The international investment community looked at Indonesia’s governance framework and said: we are not sure the rules of this game will hold. The MSCI watchlist mechanism is a formalized trust signal. It is the index provider, acting as proxy for the global institutional community, saying: we are uncertain whether the rules of this market will be reliably enforced.

That single judgment was worth $80 billion.

The NBER paper by Burnham, Gakidis, and Wurgler studied 17 MSCI reclassifications between 2000 and 2015. The pattern is consistent. When a market moved to a less-benchmarked index, the average return between announcement and effective date was negative 12.5%. In the year after the effective date, positive 23.3%. The mirror image held for upgrades: a 23.2% run-up before the effective date, then negative 12.4% in the year after. Prices overshoot on flow pressure. Then they revert. The long-run return is roughly flat.

For the Philippines, Jakarta is not a spectator event. Every emerging market is constantly managing the trust premium embedded in its cost of equity. If the Philippines were placed on the MSCI watchlist tomorrow, there is no reason to believe the pattern would be any different. The question is whether the market is prepared.

These two words are routinely conflated. The conflation leads to bad analysis and worse investment decisions.

Governance: The Architecture of Accountability

Governance is a formal system. It is the set of rules, structures, incentives, and enforcement mechanisms that determine how decisions are made and how power is constrained. At the company level: the board, the audit committee, related-party policies, the compensation structure. At the market level: the regulatory regime, SEC enforcement credibility, legal protection of minority shareholders, and disclosure standards.

Governance exists to solve the principal-agent problem. Fund managers are principals. They entrust capital to company managers, who are agents. The governance system is supposed to ensure those agents act in the principal’s interest rather than their own. When governance fails, value leaks. Sometimes slowly, through excessive compensation and empire-building. Sometimes catastrophically, through fraud.

Trust: The Market’s Confidence the Architecture Works

Trust is not a formal system. It is an expectation. Guiso, Sapienza, and Zingales, in their 2008 paper in the Journal of Finance, define trust as the subjective probability that an investor attributes to the possibility of being cheated. Not the actual probability. The perceived probability. That perception is shaped by culture, history, personal experience, the news cycle, and what happened to your neighbor.

Sapienza puts it simply: for many people, the stock market is not different from a three-card game played on the street. They need to trust the fairness of the game and the reliability of the numbers to invest.

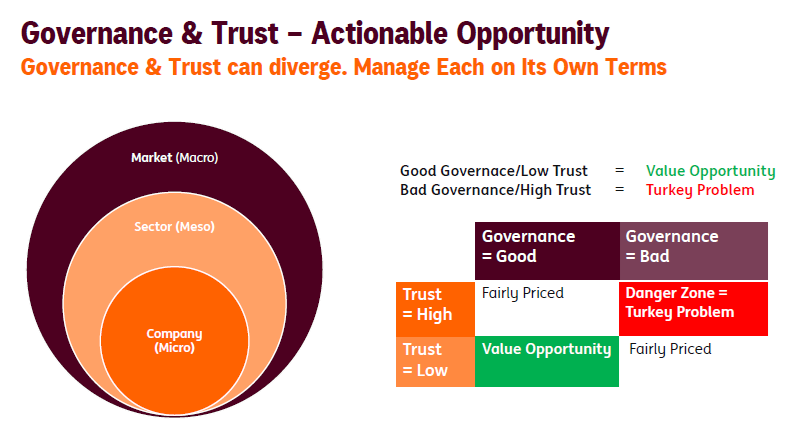

The Divergence That Matters

Governance and trust can move in opposite directions. A company can have excellent formal governance and still suffer a trust deficit, because investors believe the mechanisms will not hold under stress. Conversely, a company with mediocre governance can still command trust, because the management team has twenty years of keeping their word.

Good governance with low trust is a value opportunity. Bad governance with high trust is the turkey problem. The relationship between the two is not additive. It is multiplicative and conditional. Track both variables independently, at the company level, the sector level, and the market level.

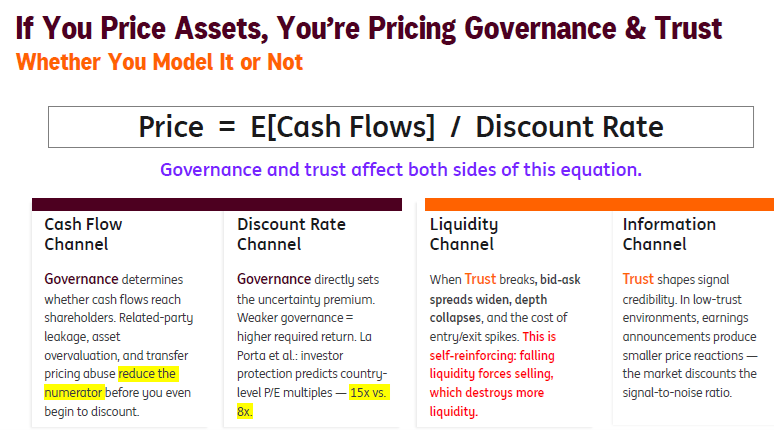

Every fundamental investor lives by one equation: price equals expected cash flows divided by the discount rate. Governance and trust affect both sides. Most investors model only one.

The Cash Flow Channel

Governance determines whether the money a business generates reaches shareholders. Related-party leakage, asset overvaluation, and transfer pricing abuse within conglomerates reduce the numerator before the discounting process begins. When SEC Chair Lim describes trillions erased, he is describing a repricing of the numerator itself.

The Discount Rate Channel

Trust directly sets the uncertainty premium. La Porta, Lopez-de-Silanes, Shleifer, and Vishny demonstrated that legal investor protection predicts country-level P/E multiples. The difference between a market that trades at 15 times earnings and one that trades at 8 times is often not about growth. It is about trust.

The Sapienza finding that should alarm every emerging market investor: trusting others increased the probability of stock market participation by 50% of the average sample probability and raised the share invested by 3.4 percentage points. This is not a marginal effect. Trust is a participation variable. It determines whether capital shows up at all. And participation determines liquidity, which determines price discovery, which determines whether a market can function as a market.

The Liquidity Channel

When trust breaks, bid-ask spreads blow out. Market depth disappears. The cost of entry and exit spikes. This is self-reinforcing. Falling liquidity forces selling. More selling destroys more liquidity. Jakarta lost $80 billion in forty-eight hours. That is the liquidity channel at work.

The Information Channel

In low-trust environments, earnings announcements produce smaller price reactions. The market discounts the signal-to-noise ratio. It learns to distrust the numbers. For fundamental analysts, this means the DCF may be built on a false numerator. The reported cash flows and the actual cash flows are different animals in weak governance environments.

Theory is useful only if it hands practitioners something they can use on Monday morning. Four tools follow. Each is drawn from a different intellectual tradition. Together, they form a system.

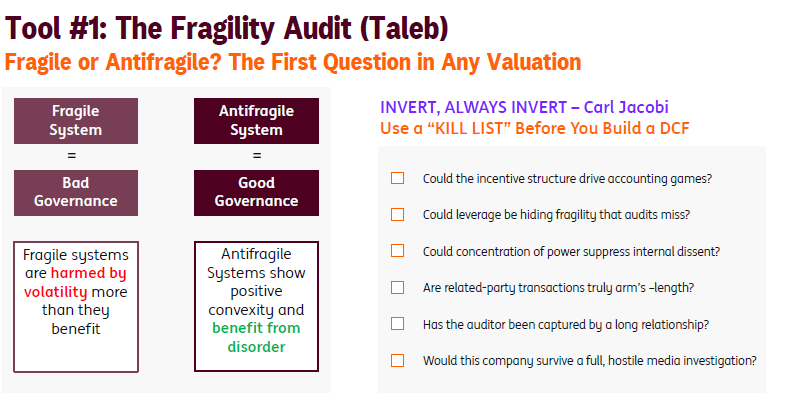

Tool One: The Fragility Audit (Taleb)

Nassim Taleb asks the central question: is this system fragile or antifragile? A fragile system is one that looks stable but carries hidden catastrophic risk. Like the turkey. Smooth earnings, steady dividends, clean audits. Everything looks fine. Until it does not. An antifragile system gains from disorder. A company that bends under stress but does not break. That gains market share when competitors fracture.

Governance determines which category a portfolio position occupies. Weak governance creates fragility: the position collects a small premium while carrying unbounded downside risk. Strong governance creates the opposite: the ability to compound through volatility rather than be destroyed by it.

The practical discipline: before building a valuation model, run the kill list. Could the incentive structure drive accounting games? Could leverage be hiding fragility that audits miss? Could concentration of power suppress internal dissent? Has the auditor been captured by a long relationship? Would the company survive a hostile front-page investigation? If these questions cannot be answered with confidence, the model that follows is built on sand.

Charlie Munger called this inversion: before you model the upside, identify what could kill it.

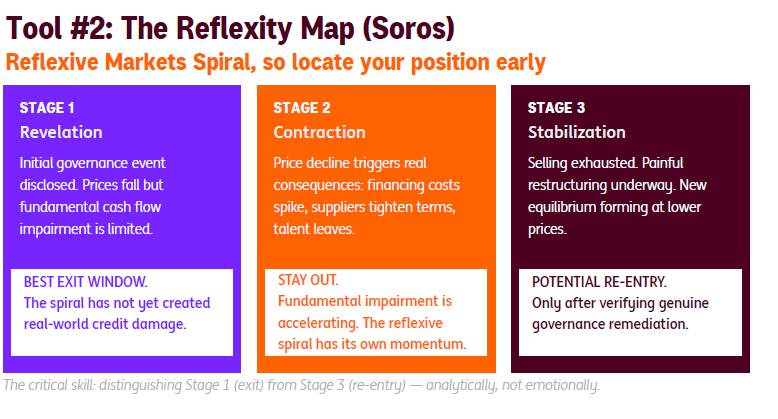

Tool Two: The Reflexivity Map (Soros)

George Soros introduced a concept the academic world spent decades ignoring: reflexivity. Markets do not just observe reality. They shape it. Prices influence the fundamentals that are supposed to determine prices.

In a governance crisis, reflexivity operates in stages. Stage one: a problem is revealed. Prices fall, but the real damage to cash flows is still limited. Stage two: the falling stock price raises the company’s cost of borrowing. Suppliers tighten terms. Talent starts to leave. Stage three: those real-world consequences impair actual operations. Stage four: the operational impairment validates the original concern. Stage five: more selling. The spiral feeds itself.

Jakarta followed this sequence in real time. MSCI raised a flag. Stocks fell 7%. Goldman and UBS downgraded. The rupiah weakened. The weaker currency raised import costs. The reflexive cycle was running before anyone finished reading the press release.

The key skill is knowing where you are in the cycle. Stage one is the best exit window. The spiral has not yet done real-world damage. Stage two, stay out. The reflexive momentum has its own physics. Late stage three is where patient contrarians look for re-entry. But only after independently confirming genuine governance remediation.

The insight most investors miss: once a market shifts from a regime of trust to a regime of suspicion, every piece of good news gets dismissed as spin. Every ambiguous signal is interpreted as confirmation of the worst case. That regime shift is the single most dangerous dynamic in emerging market investing. The question is never ‘is this priced in?’ The question is ‘where in the reflexive cycle are we?’

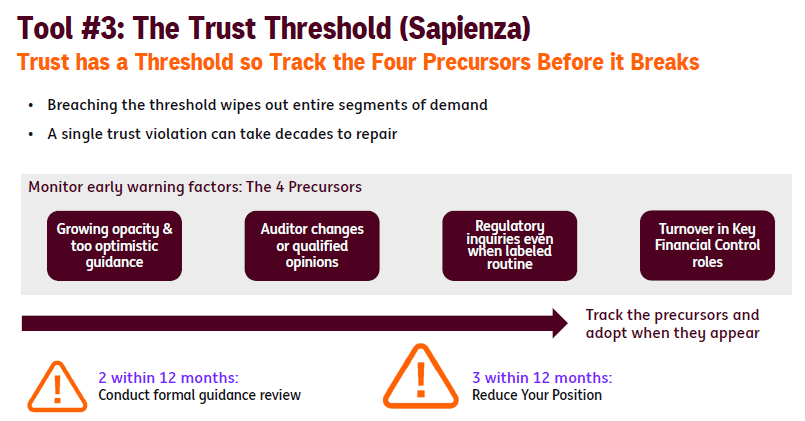

Tool Three: The Trust Threshold (Sapienza)

Sapienza and her co-authors identified something that changes how investors should think about market crashes. Trust has a threshold effect. Investors enter the stock market only if their personal trust exceeds a minimum value. Below that threshold, they hold zero equity. Not less equity. Zero.

This is why governance scandals produce collapses, not gradual adjustments. When a scandal pushes the market’s trust perception below the threshold for marginal investors, those investors do not slowly reduce their allocation. They leave. The demand curve does not shift left. A segment of it disappears entirely.

The cost is staggering. Sapienza’s team calculated that it takes 81 years of clean data to convince an investor with a 4% perceived probability of being cheated to come back. Eighty-one years. And that number assumes the investor trusts the data itself. People who have been cheated do not just distrust the company. They distrust the evidence that the company has changed.

The practical discipline: track four precursors of trust collapse. One, increasing opacity in disclosures and management guidance that is consistently too optimistic. Two, auditor changes or qualified opinions, especially with explanations that minimize the significance. Three, regulatory inquiries, even when management characterizes them as routine. Four, turnover in key financial control roles: the CFO, the internal audit head, the external auditor relationship partner.

Two precursors within twelve months should trigger a formal governance review. Three should trigger a position reduction. Regardless of the valuation.

Tool Four: The Character Screen (Buffett and Munger)

Warren Buffett stated it plainly: when we hire people, we look for intelligence, energy, and integrity. Without the last one, the first two will destroy you.

Charlie Munger went further. The most dangerous investment mistakes are not errors of analysis. Not a missed competitive moat. Not a wrong discount rate. The most dangerous mistakes are mistakes of character assessment. Backing a management team with compromised integrity destroys the principal, not just the return.

Build a formal character assessment for every significant holding. Track record of doing what they said they would do. How they handle bad news. Whether they bury problems in footnotes or address them head-on. How they treat the listed company’s balance sheet. Whether related-party behavior shows discipline or extraction. How they respond to regulatory scrutiny.

Score it. Weight it. Track it over time. When the score shows a trend of deterioration, that is a leading indicator. It will show up in the financials later. But by then, the reflexive cycle may already be running.

When these four tools are laid side by side, a unified causal chain emerges that explains every major governance-driven market event in recent memory.

Weak governance creates distorted information signals. Distorted signals attract capital on false premises, building invisible fragility. When the distortion is revealed, the market’s reflexive mechanisms kick in, accelerating the repricing beyond what fundamentals alone would justify. And the repricing is fat-tailed: not a smooth correction, but a discontinuous collapse that destroys value on a scale that standard models cannot anticipate.

Governance is the incentive architecture of capital. Trust is the coordination mechanism of markets. When incentives distort and coordination breaks, reflexivity accelerates fragility, and the repricing is nonlinear. This is the causal chain that explains Jakarta. That explains Wirecard. That explains Credit Suisse. That explains every governance-driven market event in history.

The Philippines is at an inflection point. SEC Chair Lim’s enforcement posture is a positive signal. But Jakarta demonstrates the speed and magnitude of the downside when the signal breaks. $80 billion in two days. For this market, the question is not whether governance matters. The question is whether it is being measured with the same discipline applied to DCF models.

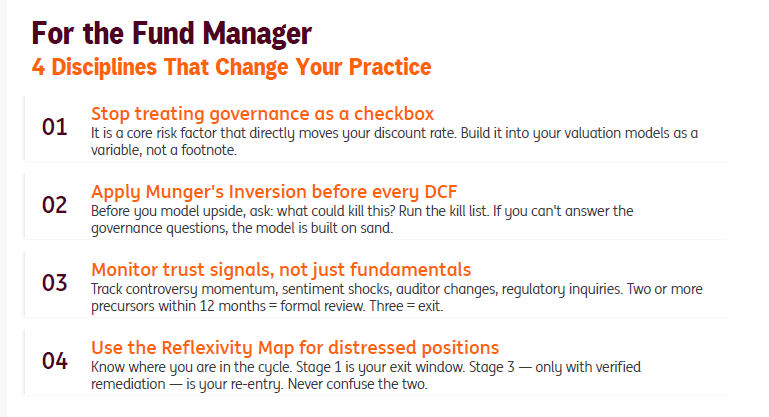

Four disciplines for integrating credibility pricing into daily fund management:

First, stop treating governance as a checkbox. It is a core risk factor that directly moves the discount rate. Build it into valuation models as a variable, not a footnote.

Second, run the kill list before every valuation. If the basic integrity questions cannot be answered, do not model the upside.

Third, monitor trust signals alongside financial statements. Track auditor changes, regulatory inquiries, disclosure opacity. Two precursors in twelve months means a formal review. Three means exit.

Fourth, use the reflexivity map for distressed positions. Know where you are in the cycle. Stage one is the exit window. Stage three, only with verified remediation, is the re-entry point. Never confuse the two.

• • •

Trust is a balance-sheet item. Markets just do not book it until it is gone.

• • •

Buy robustness. Short fragility. Build the toolkit. Track the precursors. Know where you are in the cycle. And when the early signals of trust recovery appear in this market, act before the consensus catches up.

The investors who understand trust as a measurable, trackable variable will see opportunities that the purely quantitative investor will miss. And they will avoid catastrophes that the purely narrative investor will walk straight into.

About the Author and This Series

Philip Te is a capital markets practitioner and the founder of www.johnphilipte.com. This article is the first in a series on governance and trust as pricing variables. The second article will formalize the Trust Velocity Indicator. The third will apply the reflexivity map to live case studies, including the Jakarta reclassification trade. Philip is developing these ideas into a formal paper and a masterclass for institutional investors.