Forget First Principles. Start With the Mess

How a structurer's first mental model — breaking complex things into simple parts — created McNuggets, built Dell, unlocked billions in hidden value, and helped me lose 30 kilograms.

Generated by AI

"A chicken is not a chicken. A computer is not a computer. A company is not a company. Everything complex is just simple things combined — and the person who sees the parts before the crowd sees the whole, wins."

The McNuggets Problem

In 1983, McDonald's had a problem. They wanted to launch the Chicken McNuggets nationwide after seeing its early commercial success in a small location. The product is deceptively simple: take chicken, bread it, fry it, put it in a box. But the economics were not simple.

To launch a nationwide menu item, McDonald's needed a fixed-price chicken contract from their producers. This is where it gets tricky. No producer would give them one.

Why? There is no chicken futures market. The cost of raising chicken is volatile. Feed prices swing with the grain markets. Energy costs fluctuate with oil. A farmer who locks in a fixed price is effectively betting that input costs will not spike. If they do, the farmer loses money on every chicken committed to sell. No farmer would take that risk.

And so — the McNuggets was stuck.

Enter Ray Dalio. He was not the billionaire hedge fund manager then. He was a commodity risk advisor, brought in on consulting work to help farmers solve the McNuggets puzzle. And Ray Dalio did something nobody else in the room had thought to do.

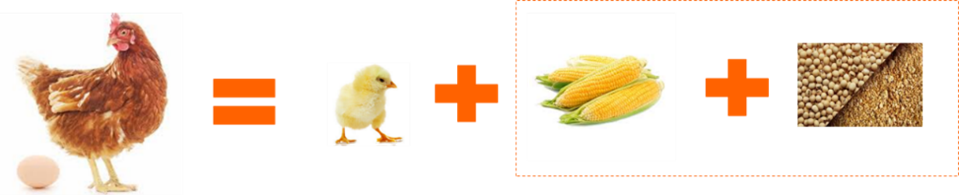

He stopped looking at the chicken.

Dalio's insight was that a chicken is not a chicken. Or rather — a chicken is not one thing. It is many things combined. A chicken (it sounds cruel to say this) is a biological machine. It is composed of a small chick — little or no value at the start — and the present value of the cost to raise it. The bulk of the economic cost of a chicken comes from the cost to raise it.

This is game changing. First, those inputs are identifiable: corn, soybean meal, a small amount of energy, and relatively stable labour. And better news — those are hedgeable: corn has a futures market. Soybeans have a futures market. Energy has a futures market.

So while there is no futures market for chicken, there is a futures market for everything a chicken is made of.

Dalio created a synthetic chicken price. He combined corn futures, soybean meal futures, and a small energy component into a contract that tracked the cost of producing a chicken. This enabled the producer to lock in input costs. And because of that, McDonald's could lock in a supply price.

The McNuggets launched. It became one of the most successful product introductions in fast food history.

This was a triumph of financial engineering. And the lesson at its core is devastatingly simple: a complex thing was actually a combination of simpler things.

This is the mindset of decomposition.

What Is Decomposition?

Decomposition is the structurer's first mental model, and it is the foundation on which all others stand.

The principle: every complex problem is a combination of simple problems. The structurer's first move is always to break it apart.

This sounds obvious. It is not. Most people, when they encounter something complex, try to understand it whole. They stare at the complete picture and attempt to process all of it at once. This is like trying to eat an elephant in a single bite.

The structurer does the opposite. The structurer refuses to be intimidated by the complexity of the whole until each part has been identified and understood.

The path to understanding the whole always runs through the parts. Like Ray Dalio — he did not attempt to understand chicken pricing by studying chicken pricing. He understood it by studying corn, soybeans, and energy. The chicken was the last thing he looked at.

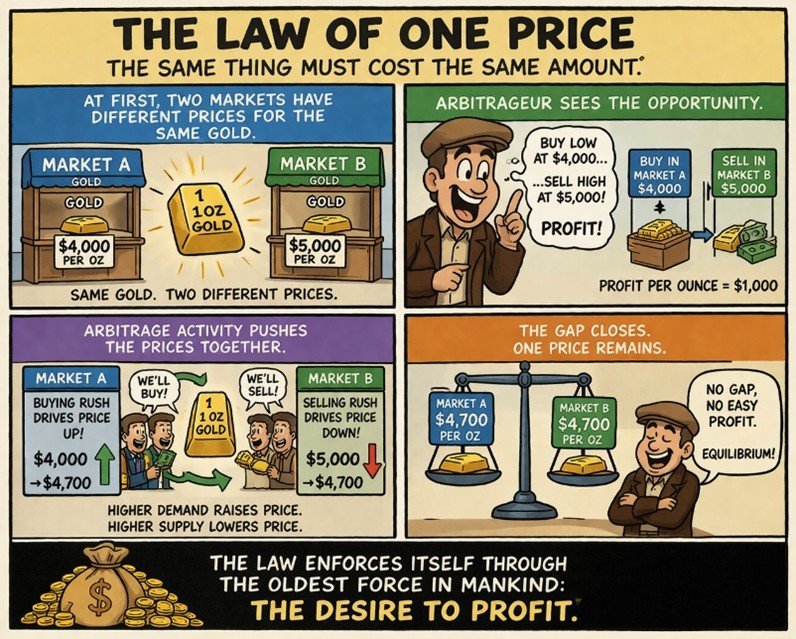

The Intellectual Foundation: The Law of One Price

The intellectual bedrock of decomposition comes from one of the most foundational ideas in finance: the Law of One Price. This law is so simple it sounds obvious, and yet it underpins trillions of dollars of financial markets activity every single day.

The Law of One Price says: the same thing must cost the same amount. If an ounce of gold costs $4,000 in one market and $5,000 in another, someone will buy at $4,000 and sell at $5,000. Every time they buy at $4,000, they push the price up (higher demand). Every time they sell at $5,000, they push the price down (higher supply). Eventually the two prices meet. The gap closes. The law enforces itself through the oldest force in mankind: the desire to profit.

Economists call this arbitrage — the act of exploiting price differences for riskless gain. And the Law of One Price is just the conclusion we expect after arbitrage has done its work.

Now imagine someone hands you a complicated object and asks: what is this worth?

Imagine that this complicated thing is actually just three simple things combined together. And you already know the price of each simple component. You add them up. There — you have your answer.

This is decomposition. You break the complex into simple, value each piece, and reassemble.

What gives you the confidence to do this? The Law of One Price. If the whole can be broken into parts, and you can price each part separately, then the whole must equal the sum of its parts. If it doesn't? Then someone will break it apart (or reassemble it) and collect the difference as profit.

Decomposition in Practice: Three Principles

Whenever you face a complex problem — in finance, in business, and in life — decomposition asks you to do three things:

1. Ask: Can I break this into simpler parts that I already understand?

2. Reflect: Do the parts add up to the whole? If not — why not?

3. Act: Identify and close the gap between price and value.

Let me show you each one.

Principle 1: Break It Into Parts You Already Understand

The Dell Case Study

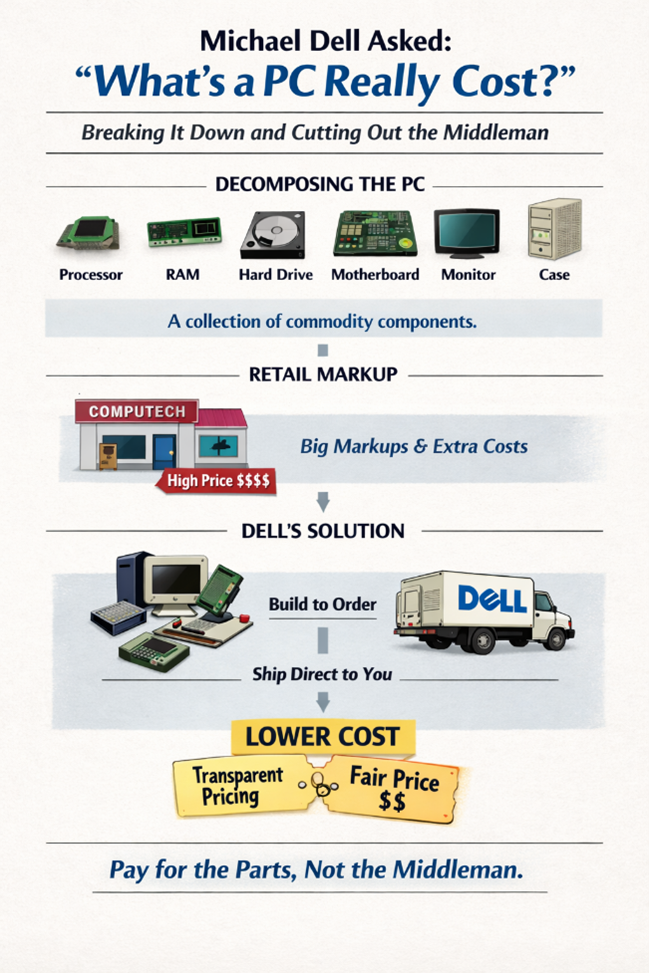

In 1984, a nineteen-year-old freshman at the University of Texas at Austin asked the decomposition question about a personal computer — and dropped out to pursue the answer.

Michael Dell looked at an IBM PC selling for $3,000 at a retail store and saw something the industry had trained everyone not to see. He saw a collection of commodity parts: an Intel processor, memory chips, a hard drive, a standard motherboard, a monitor, a case. Every one of those components could be purchased on the open market at a known, transparent price. And when Dell added up what the parts actually cost, the total was a fraction of what the customer was paying.

The gap between the component cost and the retail price was not value. It was friction. It was Compaq's factory overhead, assembling machines to forecast rather than to order. It was inventory sitting in warehouses and on retail shelves, depreciating in an industry where component prices fell by the month. It was the retailer's margin — the cost of shelf space, sales staff, and a showroom. None of these things made the computer faster, more reliable, or more useful. They just made it more expensive.

Dell's move was pure decomposition. He broke the PC into its constituent parts, priced each part at its commodity cost, reassembled to the customer's exact specification, and shipped direct. No warehouse. No retailer. No forecast-driven inventory.

By eliminating every layer of friction between the component and the customer, Dell could offer a better machine at a lower price — and still earn a healthy margin, because his costs were genuinely lower, not just squeezed.

Within a decade, Dell Computer Corporation was one of the most valuable technology companies in the world.

The lesson is not about computers. The lesson is about seeing. Most people looked at a PC and saw a finished product — a single, indivisible thing with a price tag. Dell looked at a PC and saw an assembly of known parts with known prices, bundled together with a large and unnecessary markup. The first person sees a thing. The second person sees a structure.

Decomposition is the discipline of always being the second person.

Principle 2: Do the Parts Add Up to the Whole?

The Wendy's and Tim Hortons Decomposition

Once you've decomposed something into its parts, the next question is mathematical: does the sum of the parts equal the price of the whole? If it does, the market is functioning. If it doesn't, something interesting is happening — and you need to figure out whether the gap represents an opportunity or a trap.

One of the most dramatic examples of this gap in modern financial history played out not in the abstract world of derivatives, but in the very concrete world of hamburgers and Canadian doughnuts.

In 2005, Wendy's International was a sprawling restaurant conglomerate trading at around $45 per share. It owned the Wendy's hamburger chain, Tim Hortons (a Canadian coffee and baked goods brand growing at an extraordinary pace), Baja Fresh, and Café Express.

The market was pricing Wendy's as a single entity — one stock, one price, one story.

A thirty-nine-year-old hedge fund manager named William Ackman looked at that single stock and performed a decomposition.

Ackman broke Wendy's into its component businesses and valued each one separately. Tim Hortons' revenues had grown by 53% between 2002 and 2004, versus Wendy's own 21%. Hortons generated strong free cash flows and commanded a premium brand position in Canada. Baja Fresh, by contrast, was losing money per store.

When Ackman valued each division independently — using discounted cash flow analysis and comparable company multiples — he arrived at an intrinsic equity value of $60 to $70 per share. The stock was trading at $45. The market was undervaluing Wendy's by 25% to 46%.

But here was the crucial insight: the undervaluation wasn't because any single division was mispriced. It was because the conglomerate structure itself was destroying value.

Tim Hortons' extraordinary growth was being averaged down by Wendy's struggling core business and the failed Baja Fresh experiment. Investors looking at the combined entity saw a mediocre restaurant company. Ackman, looking at the decomposed parts, saw a world-class growth brand trapped inside an underperforming holding company.

His proposal was elegantly simple: separate the parts. Spin off Tim Hortons.

The market agreed with the decomposition. On July 29, 2005, when Wendy's announced its intention to pursue Ackman's recommendations — including an IPO of Tim Hortons — the stock jumped 13% in a single day.

The Tim Hortons IPO debuted on March 24, 2006, and shares soared nearly 22% on the first day. Within a year, Hortons' market capitalisation stabilised at $6.3 billion — three times the value of the remaining Wendy's. The part that had been hidden inside the whole was, once liberated, worth far more than anyone paying attention only to the whole had realised.

Ackman's edge was not superior intelligence. It was decomposition — the willingness to take the bundle apart, price each piece, and notice that the sum of the parts was dramatically greater than the price of the whole.

Principle 3: Close the Gap Between Price and Value

The third principle is the deepest move, and it elevates decomposition from intellectual exercise into practical action. It also became the foundation of one of the most enduring investment philosophies of our time — value investing.

Benjamin Graham: The Father of Value Investing

Graham, widely regarded as the father of value investing, performed what may be the most consequential — and profitable — decomposition in the history of finance. Not of a company, but of the philosophy of investing itself.

He broke it into two components that most people confuse for the same thing but are, in fact, entirely different:

Price and Value.

Price is what you pay. Value is what you get.

Price is what the market quotes you on any given day. Value is what the underlying business is actually worth — the present value of the cash flows it will generate over its lifetime.

Graham's insight was that these two things are related over the long run but can diverge wildly in the short run. And understanding why they diverge is the key to making money — and the key to not losing it.

To explain the divergence, Graham invented one of the most powerful metaphors in the history of economic thought: Mr. Market.

Imagine that you own a share of a business with a partner called Mr. Market. Every day, Mr. Market shows up at your door and offers to buy your share or sell you his. The trouble is that Mr. Market is emotionally unstable. Some days he is euphoric and offers a wildly high price. Other days he is despairing and offers to sell at a fraction of what the business is worth. You are under no obligation to trade with him. You can simply wait.

The genius of this metaphor is that it decomposes the stock market itself into two components: a weighing machine and a voting machine. In the short run, the market is a voting machine — it reflects popularity, mood, momentum, fear, and greed. In the long run, it is a weighing machine — it reflects the actual economic value of the underlying business.

The decomposition of investing, then, is this: separate the signal (value) from the noise (price), and act only when the gap between them is large enough to provide what Graham called a margin of safety.

Graham assumed that cash flows could be estimated conservatively, that Mr. Market's moods would eventually correct, and that patience was a competitive advantage. These assumptions were sound — and they made him, and his greatest student Warren Buffett, extraordinarily wealthy.

Decomposition Beyond Finance: Naval Ravikant's Life Formulas

Everything I have told you so far has been about markets and companies and prices. But decomposition is not a finance technique. It is a way of thinking — and the most interesting thinkers in the world apply it to everything.

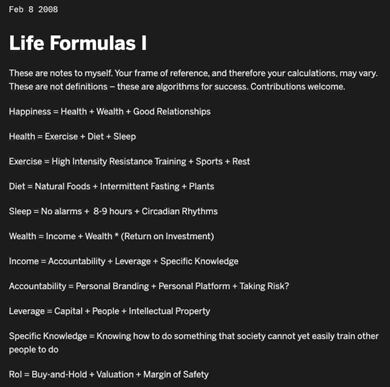

One of the best applications came from Naval Ravikant — the philosopher-investor who took decomposition and applied it to the biggest question of all: how do you build a good life?

Most people treat happiness as a single, vague, undecomposable thing — something you either have or you don't. Naval refused this framing. He decomposed it:

Happiness = Health + Wealth + Good Relationships

Already, this is powerful. Happiness is not one thing. It is three things. And because it is three things, you can work on each one independently. You don't need to solve all of life at once. You need to identify which component is weakest and strengthen it.

But Naval didn't stop there. He decomposed each component further:

Health = Exercise + Diet + Sleep

And each of those decomposed again:

Exercise = High Intensity Resistance Training + Sports + Rest

Diet = Natural Foods + Intermittent Fasting + Plants

Sleep = No Alarms + 8–9 Hours + Circadian Rhythms

For Wealth:

Wealth = Income + Wealth × Return on Investment

Income = Accountability + Leverage + Specific Knowledge

Accountability = Personal Branding + Personal Platform + Taking Risk

Leverage = Capital + People + Intellectual Property

Specific Knowledge = Knowing how to do something society cannot yet easily train other people to do

Return on Investment = Buy and Hold + Valuation + Margin of Safety

Look at that last line. Naval's formula for return on investment ends with valuation and margin of safety — Benjamin Graham's own terms. The decomposition of life, carried far enough, arrives at the same principles as the decomposition of markets. The tools are universal.

What Naval has done is exactly what Dell did to a computer, what Ackman did to Wendy's, what Graham did to investing. He took a complex, overwhelming, apparently irreducible thing — a good human life — and broke it into parts that can be individually understood, measured, and improved.

You cannot wake up tomorrow and "be happy." That instruction is useless. But you can wake up tomorrow and do high-intensity resistance training, eat natural foods, sleep eight hours, build a personal platform, take a risk, and invest with a margin of safety.

Decomposition gives you the motivation and courage to take action. Each of those is a concrete, actionable component. Each one moves the whole forward.

Personal Story: How I Decomposed Obesity

For most of my adult life, I was obese.

I am a senior banker. I run teams across Asia. I read voraciously, write constantly, and pride myself on disciplined thinking.

But when it came to my own body, I was a conglomerate trading at a massive discount to intrinsic value — bundled together with bad habits, blended averages, and a management team (me) that had been misallocating resources for years.

I had tried every crash diet. Every quick fix. Every dramatic resolution on January 1st. I would lose weight for three months, then gain it back. The pattern was as predictable as a mean-reverting stock price. I was, in Graham's language, a voting machine — reacting to mood, momentum, and short-term emotion — when what I needed to be was a weighing machine.

Then one December, my daughter was hospitalised. I accompanied her and did not eat for twenty-four hours. And in that involuntary fast, something shifted. For the first time in my life, I knew what it felt like to be genuinely hungry — not bored, not stressed, not socially pressured to eat. Actually hungry.

I had been a mindless eater my entire life. That night in the hospital, I discovered I had been confusing noise for signal. I had been eating in response to everything except hunger.

That was my catalyst. Like Ackman buying his first call options on Wendy's, it was the moment the thesis became a position.

But a catalyst without a method is just emotion. And emotion fades. So I did what I now teach: I decomposed the problem.

Step One: I Broke Obesity Into Its Component Forces

A book called Change Anything by Kerry Patterson — purchased used for SGD 2.90 — gave me the framework. The authors made a claim that stopped me cold: there is only one way to succeed at lasting change, but there are endless forces that cause you to fail. Work dinners. Travel. Hawker food. Weekend indulgence. Snacking. Lack of sleep. Peer pressure. Hotpot. The forces against you outnumber the forces for you.

You are, to borrow the language of this article, a conglomerate where the struggling divisions are cross-subsidising the healthy one into oblivion.

This was my analytical opacity moment. I had always thought of my weight as one problem. Patterson taught me it was many problems — a portfolio of forces, each operating independently, each requiring its own strategy. I had been applying a single blended solution (willpower) to a multi-segment challenge. No wonder it failed. You cannot fix a conglomerate with a single initiative. You need a strategy for each division.

Step Two: I Valued Each Component and Designed a Strategy for Each

I identified the six forces that most influenced my weight — and I built a specific, independent strategy for each one. I gave it an acronym so I would remember it: SIMPLE.

S — Snacks: Eliminate. A client once told me that the key to his physical transformation was one word: eliminate. Not moderate. Eliminate. I stopped snacking entirely. To remove the temptation, I restructured my afternoons — scheduling meetings during the hours I used to graze. This was my version of Dell eliminating the retailer. I didn't try to make snacking healthier. I removed the layer entirely.

I — Ignite: Find the Catalyst. The hospital night was my ignition point. But I learned to sustain it through inversion — the Munger move. I wrote in my notebook: "Default Future: I will be a health liability to my family and jeopardise everything I built. My daughter will carry the same behaviour into the next generation. My career will slow down because they will not see me as a leader." I decomposed the cost of not changing. The default future was the negative stub value — the implied price of inaction. It was horrifying.

M — Method: Apply a Framework. Two used books, purchased for less than SGD 10 combined, gave me the methodology. Change Anything gave me the six-source influence model. Bollywood Body by Design gave me something I didn't expect — a philosophy. One line from that book became my mantra: "Each transformation I have undertaken has helped me lift myself to a higher level of consciousness and understanding of where I want to go and who I am." Method without meaning is mechanics. Method with meaning is transformation.

P — Pray: Anchor to Purpose. My spiritual life became the structural foundation. I began tithing the first part of my day in prayer. I used the gym as my church. One practice that emerged was reading the scrolling Bible — no audio, just text — while running at high speed. Combining scripture, introspection, and physical exertion did something I cannot fully explain in analytical terms: it fused my body and my purpose into a single system. I ran faster and longer when I was reading than when I was listening to music. The decomposition of the self — body here, soul there, mind somewhere else — was itself the problem. Integration was the solution.

L — Leaf: Change the Inputs. Watching health documentaries and studying the work of Dr. Michael Greger, my wife and I shifted to 80% plant-based eating. This was not a diet. It was a change of inputs — the equivalent of Dell switching from expensive retail-channel components to direct-sourced commodity parts. Same function (nutrition), radically lower cost (caloric density and inflammation), better output (energy and clarity). We applied the rainbow diet. We cooked together. Our children watched us and began asking for vegetables.

E — Enjoy: Optimise for Process, Not Outcome. I stopped weighing myself obsessively. I stopped thinking about the result. Instead, I competed with myself — beating my personal record in cardio, extending my distance, improving my pace. I learned that I could run 10 kilometres in slightly over an hour. That fact stunned me. I had never imagined it was possible. But I hadn't been trying to run 10 kilometres. I had been trying to enjoy each kilometre. The outcome was a by-product of the process. Graham would have recognised this: he didn't try to predict the stock market. He tried to buy good businesses at fair prices. The returns were a by-product of the discipline.

Step Three: I Interrogated My Assumptions

My most dangerous assumption was that willpower was the primary variable. Patterson's book demolished this. Willpower is a depletable resource — it is the weakest force in the system, not the strongest. The stronger forces are structural: environment design, social influence, and pre-commitment.

So I rebuilt my environment. No fried food in the house. No more than one cup of rice. No social lunches — only business lunches. I made junk food hard to access and exercise easy to access. I scheduled fasting. I scheduled workouts. I enlisted my wife as a coach and my daughter as an accountability partner. I enrolled my son in Taekwondo so that fitness became a family culture, not a solo project.

I was building fences, reducing distance, and putting good behaviour on autopilot — the structural equivalent of Ackman refranchising Wendy's restaurants to shift from capital-intensive operations to asset-light systems that generate value with less management effort.

The Outcome

I lost more than 30 kilograms. I exited obesity for the first time in my adult life — almost a month later than my target, but I got there. My weight stabilised at a level I had not seen since my twenties.

But the weight was not the point. The point was what the decomposition revealed. When I stopped treating obesity as a single, monolithic, overwhelming problem and started treating it as a portfolio of independent forces — each requiring its own strategy, each measurable, each improvable — the problem that had defeated me for decades became manageable. Not easy. Manageable.

I wrote in my notebook at the start of the journey: "I am a person who lives intentionally and has the energy to live life to the fullest." That was my value statement — the equivalent of Graham's intrinsic value calculation. The market (my body, my habits, my default trajectory) was pricing me at a deep discount to that statement. The decomposition was my method for closing the gap.

The Toolbox: Sum-of-the-Parts Analysis

If decomposition is the mindset, then Sum-of-the-Parts Analysis (SOTP) is the master tool.

Value each division, asset, or cash flow stream of a company independently, then compare the sum to the market price of the whole. This is what Ackman did with Wendy's and what every serious value investor does with any multi-segment business.

The power of SOTP is that it forces you to see a company as a portfolio rather than a monolith.

The discipline is in being honest about each component — resisting the temptation to inflate the value of the strong division to compensate for the weakness of another, and resisting the temptation to ignore liabilities that reduce the total.

A clean SOTP requires you to account for everything: the operating businesses, the non-operating assets (excess cash, real estate, investments in other companies), the corporate overhead that would persist even if divisions were separated, and the full burden of debt and off-balance-sheet obligations. When the sum significantly exceeds the market price, you have a potential opportunity. When the market price exceeds the sum, you should ask hard questions about what premium is being assigned to synergies or management quality — and whether that premium is deserved.

Decomposition in the Age of AI

Decomposition is ancient. French economists were using it in the 1760s to analyse the grain markets. Ray Dalio used it to understand chicken as a biological machine. Benjamin Graham used it to develop his philosophy of buying stocks below liquidation value in the 1930s.

The weapon is old. But here is why it wins the new war.

We are entering a world of radical complexity — artificial intelligence rewriting industries overnight, geopolitical shocks rippling through supply chains, information abundance drowning out signal with noise. The dominant advice you will hear is to think from first principles — to strip everything back to fundamental truths and reason upward from a blank slate. That is Elon Musk's method. It is powerful. And for most of the problems you will actually face — especially in a world under constraints — it is the wrong tool.

Here is why. First principles thinking assumes you have the luxury of starting from zero. It assumes unlimited time, unlimited resources, and a blank canvas. It is the method of the inventor, the founder, the person building something that has never existed.

But most of the consequential decisions in your life will not be inventions. They will be evaluations — of a company, a deal, a strategy, a career move, a life structure that already exists in a messy, bundled, constrained form. You will not be handed a blank canvas. You will be handed a conglomerate and asked: what is this actually worth?

Decomposition is the anti-first-principles. It does not start from zero. It starts from the mess you have and works inward — breaking the existing structure into its components, pricing what is already there, and finding the value hidden inside the bundle. First principles builds up from nothing. Decomposition breaks down from everything. Both are powerful. But decomposition is the tool of the operator, the investor, the leader, the person who must make decisions under constraints — with imperfect information, limited time, existing obligations, and a world that will not pause while you reason from axioms.

And here is the deeper truth: the thinking that matters most happens under constraints. The elegant models assume frictionless markets, perfect information, unlimited capital, and rational actors. The real world gives you none of these. Dell had no factory, no retail channel, and no brand — but he had commodity components and a telephone. Ackman had a thesis but a CEO who refused his calls. Graham had a formula but a market that could stay irrational longer than he could stay solvent. I had a goal to exit obesity but an entire ecosystem — travel, hawker food, work dinners, snacking culture, sleep deprivation — designed to keep me fat.

The thinker who thrives is not the one with the cleanest model. It is the one who can decompose the messy reality into workable parts and build a specific strategy for each part, within the constraints as they actually exist. Not as they should be. As they are.